Introduction

As CKB continues to mature, we are actively advancing along our governance transition timeline. We are transitioning from the early core team-driven ecosystem bootstrapping phase toward long-term, self-sustaining decentralization.

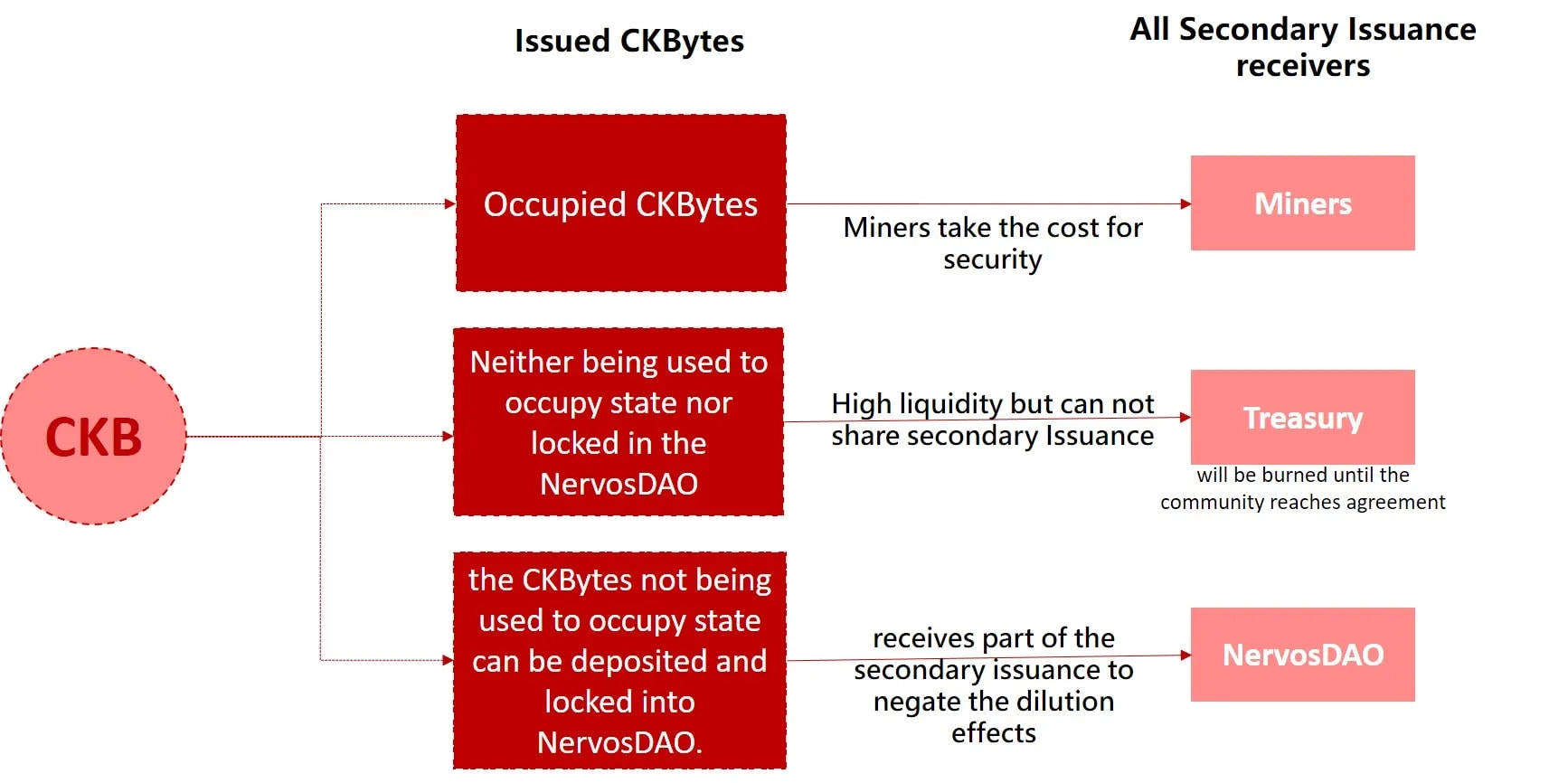

The Nervos Network uses a treasury model designed to provide sustainable funding for core development and ecosystem building.

Currently, because we haven’t built a on-chain governance mechanism, the treasury is not yet active and this portion of CKB is being “burned” (the corresponding cells are not created and no one can spend these CKB). You can find the total burnt amount on the Nervos DAO page of CKB Explorer.

Background: The CKB Secondary Issuance Model

By design, the CKB economic model features a fixed secondary issuance of 1.344 billion CKB annually. This issuance is dynamically distributed based on how the tokens are currently utilized:

In alignment with this transition, the development team is now exploring the activation of this treasury fund. The use of the treasury funds will be fully open, transparent, and verifiable on-chain for everyone to see.

However, we must emphasize the massive scope of this change. Transitioning to a fully decentralized, on-chain treasury is a monumental paradigm shift. We are currently at the very beginning of this journey, initiating discussions to lay the theoretical and technical groundwork.

Therefore, this document serves as a high-level overview of our current thoughts, the proposed scope of work, and the potential impact. We are sharing this to gather early feedback from the community, developers, and economic experts before drafting a formal RFC.

Scope of Work & Technical Direction

Activating the treasury presents a unique engineering challenge at the intersection of consensus-level and smart contract implementation. From a technical perspective, we need to implement two aspects, one is activating and storing funds, and the other is the on-chain governance mechanism.

- Modifying the “Burn” Mechanism: We need to alter the CKB protocol to redirect the currently burned secondary issuance to a designated treasury account. A critical architectural decision is whether this should be a fixed account or an account fully controlled by a smart contract. Considering a fixed account to be potentially riskier due to key management and compliance risks, we currently favor the latter option, but it’s not excluded that there could be other better options.

- Voting Mechanism & DAO Contracts: We are exploring a robust on-chain voting system and is easy for external tools (like wallets) to integrate.

- One proposal involves users minting a non-transferable sUDT (Simple User-Defined Token) as voting weight, generated from Nervos DAO deposits. Crucially, existing depositors will not need to withdraw and redeposit. Instead, they can retroactively mint voting UDTs by utilizing their current deposit cells purely as read-only “reference cells.”

- To solve the challenge of preventing double voting and improve the efficiency, we are actively evaluating Zero-Knowledge (ZK) solutions for off-chain computing paired with on-chain verification.

- We are also exploring the implementation of a delegation mechanism similar to Cardano’s DRep (Delegated Representative) system. In this model, CKB holders would not need to vote on every individual proposal. Instead, they could securely delegate their voting power to trusted community representatives without locking or transferring their actual assets. This significantly lowers the participation barrier for average users while preventing voter apathy.

- Consensus Changes: Implementing these features may require data inclusions in the block header, a targeted soft fork, or potentially a full hard fork. This is still under discussion.

In summary, we have many technical details to settle, we’ll provide more determined technical directions in the subsequent documentation.

Economic Impacts

Activating the treasury directly touches the foundational CKB economic model. We are taking this extremely seriously and plan to consult with tokenomics experts.

Currently, the burned treasury CKB acts as a passive deflationary mechanism, benefiting all current holders by keeping the circulating supply tighter. Once activated, this “burn” stops for any approved proposals. The funds will be transferred to developers, teams, or community members. This directly increases the total circulating supply of CKB in the open market.

For CKB holders who may have concerns on CKB’s inflation, here is a simplified breakdown of the math:

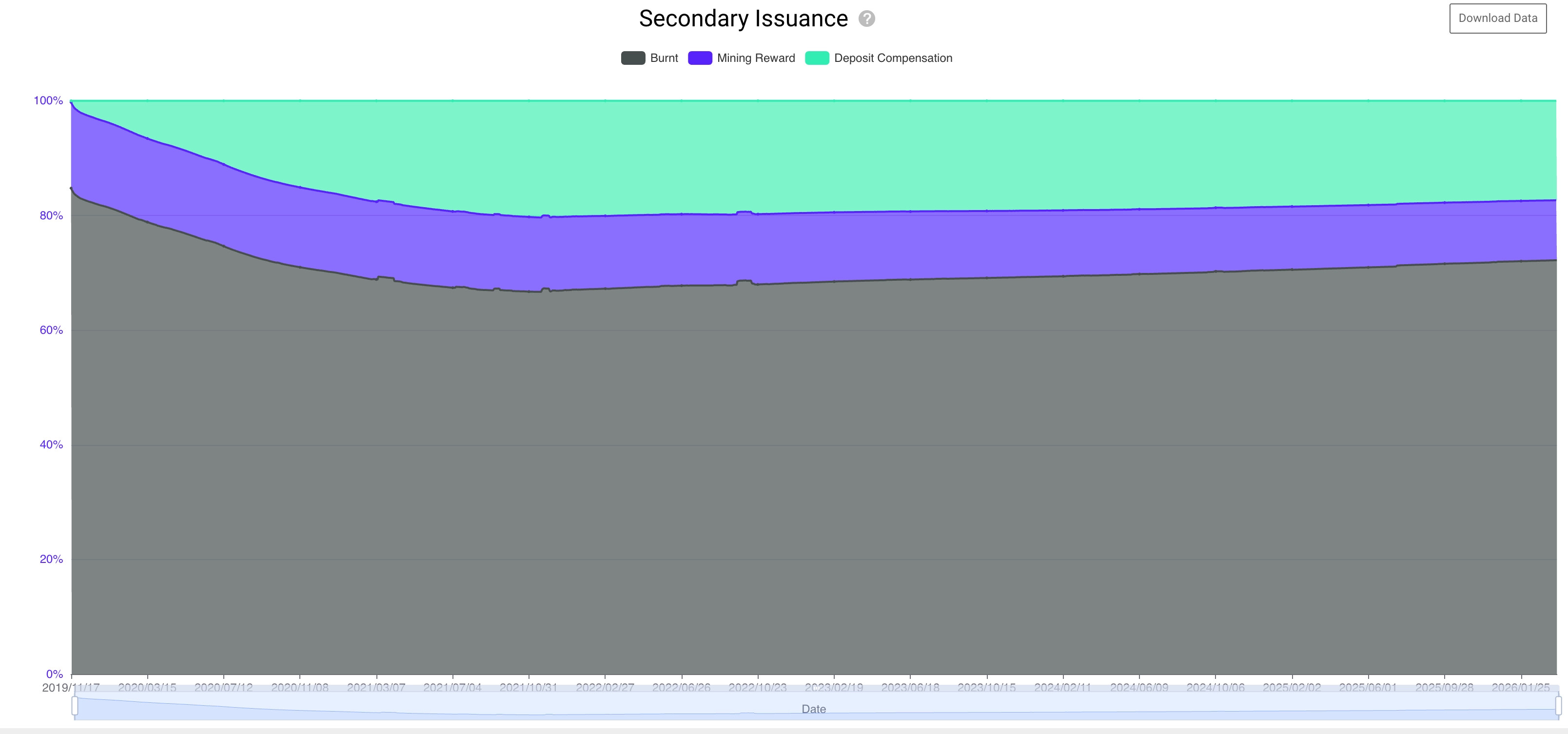

- Total Secondary Inflation: CKB’s overall secondary issuance is a fixed number: 1.344 billion, from the current statistics on CKB explorer we can see 72% of them are burnt. The secondary issuance is spread across all previously issued CKB, including the 8.4 billion CKB burned in the genesis block, leading to an issuance rate of 2.08% today.

-

The inflation caused by secondary issuance is around 0.59% per year today (~376.3 Million / 48.5 Billion of total CKB), as actually only 28% of secondary issuance contributes to real inflation, and the secondary issuance rate will continue to decrease over time. You can read more detailed explanation of CKB Issuance Model here.

-

Maximum Impact: The treasury burn accounts for about 72% of that total secondary emission today. Even if the treasury operates at maximum capacity and funds every possible proposal, it would only add a maximum of (2.08% * 72%) ~= 1.49% in annual inflation.

Therefore, the upper bound of 1.49% extra inflation is a strictly capped and predictable metric intentionally designed into the CKB economic model. While this figure is not mathematically negligible, we expect CKB voters to seriously consider whether a proposal is truly beneficial for CKB’s future, rather than rejecting it solely based on inflation concerns.

Real Inflation Mitigation for Long-Term Holders:

It is also critical to remember CKB’s unique inflation mitigation mechanism. For long-term holders who lock their CKB in the Nervos DAO, the dilutive effects of the secondary issuance are mathematically offset by the DAO Compensation Rate. Regardless of whether the Treasury funds are burned or activated, the “Real Inflation” for DAO depositors remains effectively negligible (approaching zero), providing long-term holders shelter from inflation.

Mitigating Governance Capture & Conflicts of Interest

Another concern raised by the team is the potential for governance capture. If the treasury accumulates a massive bounty of unspent CKB, it could become a “honey pot,” incentivizing malicious actors to acquire voting power simply to drain the funds.

To address this, we are strongly considering building an “option to burn” directly into the governance mechanism.

- If the community cannot reach a consensus on how utilize treasury funds, the governance protocol could direct the treasury to burn unused funds. It ensures that CKB holders only experience inflation when a proposal delivers undeniable, consensus-driven value to the ecosystem. You can join the discussion about this idea here.

Timeline & Next Steps

Our target is to finish the design, core implementation and initial testing within 1 year, leaving ample time subsequently for the community and ecosystem tools to adapt before any potential activation.

Immediate Next Steps (Pre-RFC):

- Community & Expert Review: We invite the community to review this high-level direction. We are also reaching out to economic experts to model the exact impact on the change.

- Draft Demo: Before writing a formal RFC, the development team will build a basic, functional demo to safely map out the technical intersections of consensus rules and smart contracts.

Some topics related this :