Your question is important and I think it touches a misunderstanding that deserves clarification.

TLDR; I agree that DAO depositors’ interests should be protected. But I believe they are already protected by the Nervos DAO mechanism under the normal full-secondary-issuance assumption. Redirecting unused Treasury funds to DAO depositors would go beyond protection and become an additional subsidy. That would distort governance incentives and weaken the purpose of the Treasury.

My view is that unused Treasury funds should not be redirected to Nervos DAO depositors, because it would change the meaning of both Nervos DAO and the Treasury.

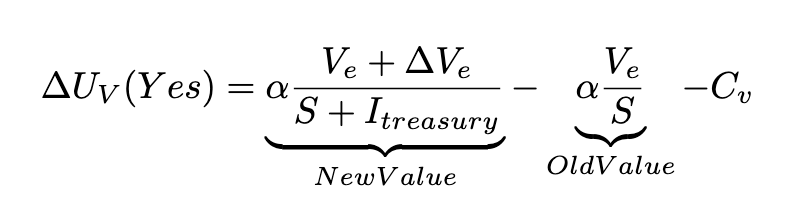

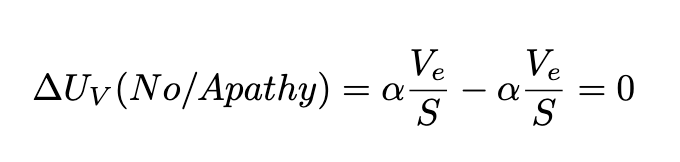

Nervos DAO was designed under the assumption that all secondary issuance is issued normally. It does not depend on Treasury burn to protect DAO depositors. Even if the Treasury portion of secondary issuance were fully issued and used, DAO depositors would still not be diluted by secondary issuance, because the Nervos DAO compensation mechanism was designed to offset secondary issuance for DAO depositors under that normal issuance model.

The current Treasury burn is therefore not part of the fundamental Nervos DAO design. It is an additional conservative choice made because decentralized governance was not ready in the early stage of the network. Since there was no sufficiently mature community governance process to decide how Treasury funds should be used, burning the Treasury portion was the safest default. This burn does have a real effect: it reduces circulating supply compared with full Treasury issuance, and therefore gives all CKB holders some extra benefit. But this extra benefit should be understood as outside the Nervos DAO design, not as something DAO depositors are entitled to receive.

This distinction matters a lot.

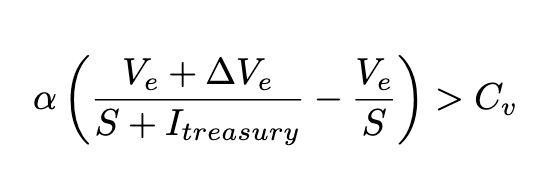

Nervos DAO is not a yield product. It is not designed to maximize APY. It is an anti-dilution mechanism for long-term holders. If we redirect unused Treasury funds to DAO depositors, then Nervos DAO would start to become something else: a yield subsidy mechanism. That would create very bad governance incentives.

Under such a model, every Treasury proposal would implicitly compete against DAO depositors’ extra APY:

If a proposal is approved, funds go to public goods.

If a proposal is rejected, funds go to DAO depositors.

This would give DAO depositors a direct financial incentive to reject Treasury spending, even when the spending is valuable for the network. It would turn Treasury governance into a conflict between public goods funding and DAO yield maximization. I think this is dangerous.

It would also create the wrong narrative for CKB. I understand why a higher DAO APY may sound attractive from a market perspective. It could look good to investors who are used to PoS staking yields. But CKB should not compete with PoS chains on yield. Nervos DAO’s strongest narrative is not “high APY”; it is:

Long-term CKB holders can avoid dilution from secondary issuance by locking in Nervos DAO.

The Treasury has a different purpose. It exists to provide sustainable support for the most essential public goods of the CKB network: core protocol maintenance, protocol research, client development, security work, infrastructure, and other work that is crucial to the long-term survival of the chain but may not have a direct business model.

This is actually one of the biggest unsolved problems in Bitcoin and Ethereum.

Bitcoin has never formed strong consensus around community governance, and it also has no native, sustainable funding source for public goods. Ethereum has spent a lot of time exploring governance and coordination, but it still largely relies on the Ethereum Foundation and related institutions for public goods funding. That dependence increases the ecosystem’s reliance on the Ethereum Foundation.

CKB is in a different position. The protocol already has a built-in funding source for public goods through the Treasury portion of secondary issuance. This is a very strong foundation. The missing piece is not the source of funding itself, but a governance mechanism that the community broadly recognizes as legitimate, decentralized, and hard to abuse.

This distinction is important. Public goods do not become sustainable simply because a community has good intentions. They require a reliable economic source that does not depend on donations, foundations, charismatic leaders, or temporary market cycles. Without economic sustainability, “decentralized governance” often becomes dependent governance in practice: dependent on a foundation, dependent on a few large donors, or dependent on whichever group happens to have resources at a given moment.

In this sense, economic sustainability is essential to the “Autonomous” part of DAO. A DAO cannot be truly autonomous if it has no native way to fund the public goods required for its own survival. What CKB still needs is a governance process that can activate and use this funding source without turning it into a rent-seeking machine. If the community can build such a mechanism — legitimate, decentralized, transparent, and resistant to capture — then CKB may have the potential to grow into one of the first truly autonomous DAOs: a decentralized network that not only governs itself, but also sustainably funds the public goods necessary for its long-term existence.

ps.

I strongly suggest the CKB community to view CKB issuance the same way as Bitcoin’s—deterministic, predictable, and effectively immutable. By “effectively immutable” I mean it should only ever change if the alternative is CKB’s demise.

This is not a dogmatic belief. It is an assumption repeatedly supported by history. A fixed issuance schedule provides the highest degree of certainty to all market participants. It gives holders, miners, developers, investors, and builders a stable reference point for valuation, planning, and long-term commitment.

More importantly, changing issuance does not only change numbers. It changes the mindset and culture of the community. Once issuance becomes a normal governance topic, people can easily become excited about whether to increase issuance by 1% or 0.5%, how to redistribute it, or which group should receive more. But this kind of discussion can distract the community from the more fundamental question: whether opening the door to issuance changes is actually beneficial to the ecosystem at all.

The damage is therefore not only economic, but also cultural. It shifts the community from building under hard constraints to debating how to relax those constraints. For CKB, I think issuance predictability should be treated as a core social invariant, not merely a configurable parameter in the protocol.

And because this invariant is ultimately protected by community consensus, not by code alone, it is especially important that the community has a correct understanding of CKB issuance, secondary issuance, Nervos DAO, and the Treasury. Code can implement the current rules, but only community consensus can decide that these rules remain legitimate and should not be changed.